{kind=link}

{kind=link}

In this project, we propose an unsupervised learning based approach for pairs selection in cryptocurrency perpetual futures market.

We first use dimension reduction and clustering algorithm to bundle assets in to each group.

Then, we use ADF test to select top cointegrated pairs from the same group.

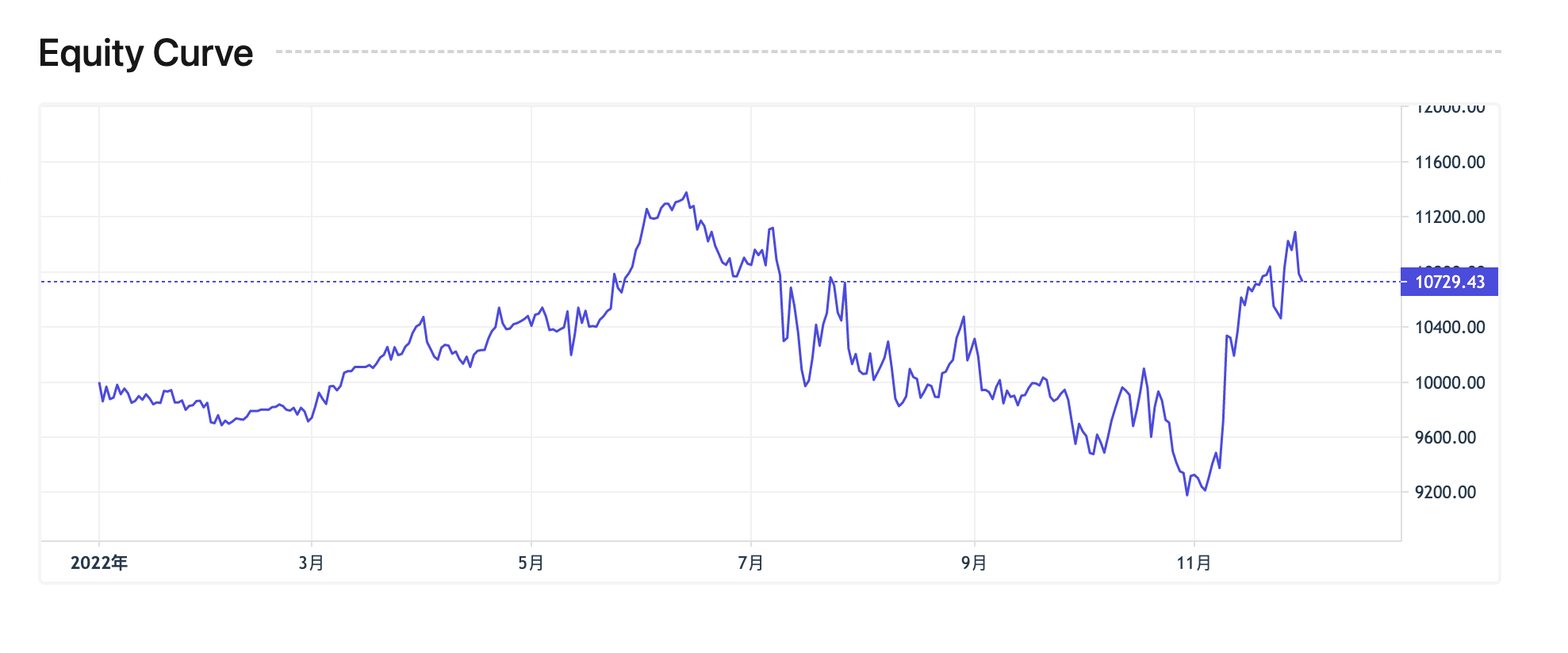

The result shows that our strategy is superior to pure cointegration testing strategy in terms of PnL (Profit and Loss) and Sharpe ratio.

See more at this report.

Our backtesting framework is Jesse Trade. The implementation of our strategy can be found in strategies/AutoPairsTrading.

Sharpe Ratio: 0.47 Annualized Return: 8%

Sharpe Ratio: 0.47 Annualized Return: 8%

Sharpe Ratio: 1.89 Annualized Return: 50.44%

Sharpe Ratio: 1.89 Annualized Return: 50.44%